Why the Markets That Overheated the Most Are Correcting First—and Why This Was Inevitable

The pandemic housing boom did not lift all markets equally. While national headlines focused on aggregate appreciation, a smaller group of metros experienced price acceleration so extreme that it detached from local economic gravity. Those same markets are now leading the national correction. This outcome is not surprising, nor is it cyclical panic. It is the predictable unwinding of excess.

During the period between early 2020 and mid-2022, housing markets such as Austin, Phoenix, Boise, and parts of the Mountain West posted appreciation rates that dramatically exceeded income growth, replacement cost economics, and long-term demand fundamentals. These gains were driven by temporary forces—ultra-cheap capital, sudden migration surges, and speculative demand responding to a perception of permanent change. Once those forces faded, prices were left unsupported at their peaks.

Austin provides the clearest illustration of this dynamic. Home values there surged more than seventy percent during the boom, only to give back roughly a quarter of that increase once financial conditions normalized. This pattern is not unique to Austin; it is simply more visible there. Markets that ran the farthest ahead of fundamentals are now the first to correct meaningfully.

The Relationship Is Structural, Not Anecdotal – Reversion to the Mean

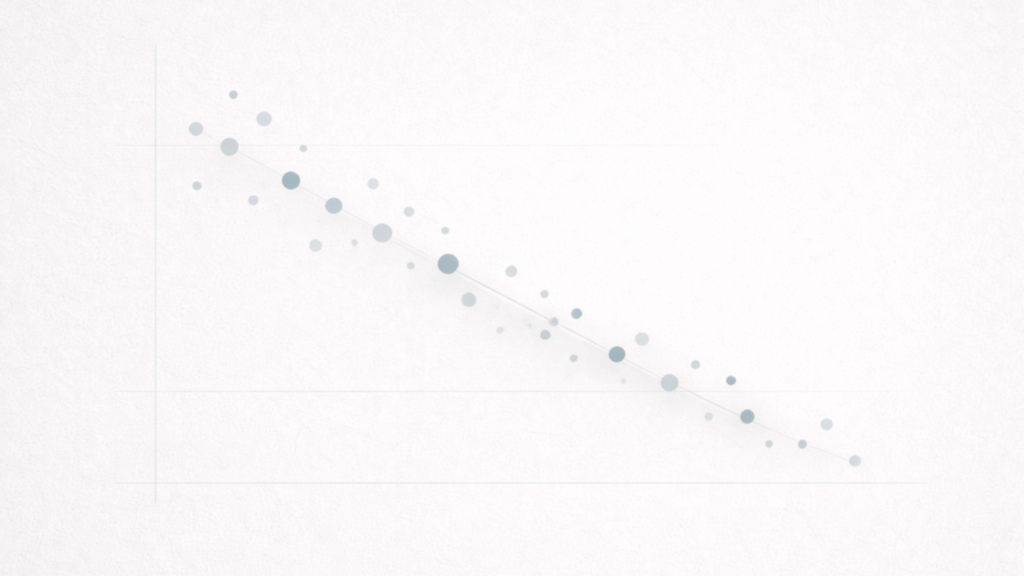

When pandemic-era price gains are plotted against post-peak price movement across major U.S. metros, a clear and consistent relationship emerges. Markets that experienced the largest appreciation during the boom are now seeing the largest declines from peak pricing. This relationship explains a significant portion of recent price movement, even after accounting for local variation.

This is not market failure. It is mean reversion—the tendency of asset prices to drift back toward levels supported by income, affordability, and demand. Housing, despite its emotional and political overlay, is not exempt from this principle.

Why This Is Not a Crash

Unlike past housing downturns, today’s correction is not being driven by systemic credit stress or forced liquidation. Underwriting standards remain materially stronger than in prior cycles, and household balance sheets, in aggregate, are not over-levered. What is occurring instead is a repricing of expectations.

Higher borrowing costs have reduced purchasing power, migration flows have normalized, and buyers are no longer willing—or able—to absorb prices that were set during a period of artificial demand. As a result, markets are transitioning from narrative-driven pricing to math-driven pricing. That transition feels abrupt in places where prices moved the fastest.

Inventory Is the Silent Accelerator

Inventory levels are quietly but decisively reshaping the balance of power across many of the markets that overheated during the pandemic. As listings rise, the seller’s ability to dictate pricing without resistance is steadily eroding, while buyers regain leverage that had been absent for years. This shift does not require economic distress, forced selling, or broad-based weakness to take hold. In housing, even modest increases in supply can have an outsized impact when demand becomes price-sensitive rather than momentum-driven. Once buyers push back, price discovery resumes.

What makes this moment particularly instructive is where inventory expansion is occurring most aggressively. It is concentrated in the same markets that experienced the greatest speculative excess—places where demand was amplified by narrative, urgency, and fear of missing out rather than by durable fundamentals. As momentum buyers step aside, listings linger longer, absorption slows, and sellers are compelled to adjust expectations. Price corrections in these environments are not sudden; they are sequential and cumulative.

This phase of the housing cycle rewards discipline, realism, and patience. Sellers must come to terms with the fact that peak-pandemic pricing reflected extraordinary conditions rather than a permanent repricing of value. Buyers must distinguish between healthy normalization and markets still resisting fundamental adjustment. Investors, in particular, must return to underwriting grounded in income growth, replacement cost, and long-term demand, rather than extrapolating short-term price trends.

The era in which housing could be priced primarily by narrative has ended. Fundamentals have reasserted themselves.

Looking ahead, the most likely path is not a national collapse, but continued bifurcation. Markets that overshot the furthest will continue to normalize over the next 12–24 months, while fundamentally constrained, supply-limited regions stabilize sooner. Price volatility will persist, but directionally, the adjustment favors balance over excess.

The housing market is not unraveling. It is recalibrating. Historically, markets that rise the fastest are the first to normalize—and those who understand that dynamic do not panic when prices adjust. They recognize the opportunity embedded in clarity and position accordingly.